A Tweet from Sam Knowlton, an American agronomist, stimulated a healthy debate at AF this week. Who is profiting from farming in 2023?

The origins of our story

A colleague shared this Tweet last week, and it got us thinking:

Obviously the US is a huge country with a highly developed agricultural sector, but these figures given by Knowlton are huge, and don’t even include fuel, power, labour etc.

Hitting pay dirt?

The comparison of farming to the gold rush is interesting, with only the shovel seller (and saloon owner, and boarding house, and horse trader and gold dealer etc etc) making any profit from the hard work panning for precious metal.

This is particularly apposite when reflecting on the news reported in AF Gleanings on 16th August that Cargill profits increased 7% in 2023, following the unprecedented increase of 23% in 2022. This was mirrored by the rest of the ‘big 4’.

Where does the UK stand?

At AF we have looked at various sources to come up with domestic figures for comparison.

We know that AF procures about 3.75% of UK fertiliser volume. Based on this we estimate UK annual spend on fertiliser is c£1.73bn.

There are no consolidated figures for seed, but we assume costs are similar to fert at c£1.5bn. (Nix gives fert:seed price ratio as 3:1 for cereals, but this is broadly reversed for potatoes, peas and beans.)

According to the Agricultural Engineers Association (AEA), annual UK machinery spend is £2.4bn.

Cost of debt based on average borrowings of £272,400 per farm (DEFRA) for 216,000 farm holdings is £2.9bn pa (assuming average interest rate of 5%).

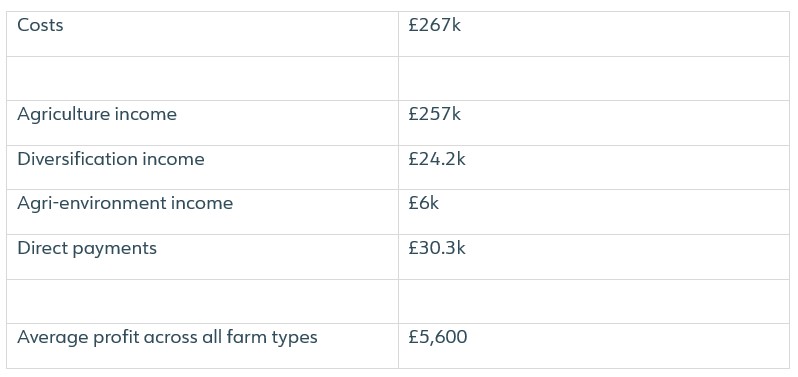

In the DEFRA presentation ‘Agriculture in the UK Evidence Pack’ (Sept 2022) the average annual gross margin before tax and salaries for all farms is £50,900.

Broken down this is:

If we work this back for the total number of UK farm holdings above, the total annual profit for agriculture is £1.21bn – less than half the cost of the total debt.

¡Ay, caramba!

Appreciating that these are estimates from a number of sources, it is hard to argue with the original contention by Sam Knowlton that there are a lot of businesses – many of them huge multi-nationals – making a lot of money on the back of farmer’s toil.

This is not to say that many are not working hard for their share, supplying valuable and important commodities. But there are some of these players who do very little but rely on the strength of Western economies, and their own freely available capital, to keep farmer profits at 2% of turnover.

Change is needed

It is really shameful that without direct payments, which contribute 54% of the gross margin, that the ‘average farm’ would make a loss. We can argue whether it is the farmer’s shame, their customer’s shame or the Government’s shame. However, for a sector which employs nearly half a million people, on 71% of the UK’s land, to be restricted to making 2% profit can not be acceptable.

Saving grace

The ray of light for farmers who own their own land, which is 54% of farms plus a further 31% of units which are mixed tenure, is the steady increase in land values. This can be the only explanation for the very high profit to loan ratios.

The current rate of increase in arable land value year to year is 4.3%, and 3.4% for pasture land. With the average farm size being 85 ha, the arable unit will have increased in value by £84,410 and the pasture land unit by £52,490, which dwarfs the £5,600 profit.

Is there a solution?

The answer of course is to reduce costs of production, and demand higher prices! AF has little control over the latter but we can help you reduce your costs.

So, whatever you are purchasing for your business, make the most of being an AF Member and #challengeAF to get you best prices.