Six month urea market overview

Urea prices spiked soon after the Russia: Ukraine conflict began due to supply concerns with Russia being one of the worlds’ biggest urea producers. Since then, prices have been easing off but easing off from high prices. Granular urea continues to be the cheapest option on a pence per kg basis and will likely be again once new season prices are released. Protected ureas which are now subject of DEFRA regulations going forward carry a £25-30/t premium but could still look competitive vs AN.

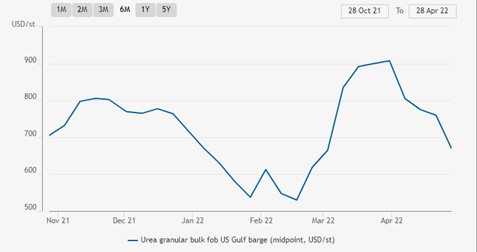

The urea market is the most volatile of the fertiliser markets. The graph below shows the urea market price from November 2021 onwards. The closure of the CF factory sparked the nitrogen market price increase for Autumn ’21. Prices then eased globally until the conflict between Russia and Ukraine in February 2022 led to record fertiliser market highs. Since mid-March, prices have eased. Factors such as the Indian fertiliser tender being smaller than anticipated have contributed to this.

Graph taken from Argus Media

Six month ammonium nitrate overview

As expected, AN followed a similar spike to urea once the Russia Ukraine conflict began. It has been the longest period of AN stability this season. We saw a >£100/t drop from CF in early Spring, dropping the market to the mid £700’s.

Gas prices have dropped and stabilised. However, with a limited AN supply after the banning of Russian AN imports, UK importers may be forced to pay prices comparable with other markets to compete for the product supply.

The graph below shows a steady increase in ammonium nitrate prices since the CF plant closure in Autumn 2021. The high gas prices kept ammonium nitrate at a steady high until the beginning of the conflict in Ukraine which led to a spike in April 2022. This is largely attributed to the reduction of Russian gas and ammonium nitrate supply. Since then, prices have dropped to pre-conflict levels.

Graph taken from Argus Media

P & K

Phosphates continue to firm on a similar curve throughout the 2022/23 season and with no export of Russian or Chinese DAP, prices continue to rise. Potash is the nutrient that is currently experiencing an uplift in price. This is due to exporters being offered higher price levels elsewhere in the world so UK importers are having to meet supplier demands.

Many growers took the decision to take PK holidays in 2021, but this is not a sustainable tactic. Even more than usual, soil testing is a recommended practice. Use soil nutrient tests to understand your exact nutrient requirements for the next growing season and tailor your nutrition programmes to maximise return on investment and to best prepare to hit optimum yields.

Your AF Fertiliser team is here to help. Speak to us on 01603 881937 or email fertiliser@af.farm.